|

|

| Getting The Most Out Of Your R&D Tax Credit Claim |

|

By

Ken Hardy, Partner, KPMG

Feb 17, 2015 |

|

|

Whether you’re already claiming the R&D tax credit or just considering your eligibility, it’s essential to remember that R&D doesn’t just happen in the laboratory – quite often it’s the work a company would consider to be a day-to-day activity: developing a new product; devising or making improvements to a production process; trying out a new material to reduce costs. The list is extensive, and with a potential saving of up to 25% of qualifying expenditure, it’s worth checking if your activities meet the criteria.

Overview of the R&D tax credit

The R&D tax credit was first introduced in 2004 and since then has been amended and generally enhanced with each subsequent Finance Act.

The tax credit operates on a group basis and is available to companies, within the charge to Irish tax, that undertake R&D activities in the European Economic Area (EEA). In the case of an Irish tax resident company, the credit is available only if the expenditure on the R&D is not otherwise available for a tax benefit elsewhere.

You could be entitled to a cash refund from Revenue worth 25% of your qualifying R&D spend

10 Key Facts

- The R&D tax credit is worth up to 25% of qualifying expenditure.

- For periods ending prior to 01/01/2015, the credit is typically claimed on incremental qualifying expenditure over the amount spent on R&D activities in the base year (i.e. an accounting period ending in 2003).

- Companies can avail of a volume-based regime (i.e. a 25% credit for every euro incurred) on the first €300,000 of qualifying expenditure for periods commencing between 01/ 01/2014 and 31/12/2014; the regime is entirely volume- based for periods commencing on/after 01/01/2015 (i.e. no requirement to deduct base year expenditure).

- This credit is available in addition to the trading deduction available for R&D spend. For a 12.5% taxpayer, this can result in a net subsidy of 37.5% (i.e. 12.5% corporation tax deduction + 25% R&D tax credit).

- Expenditure met by grant assistance received from the State, the EU, or EEA does not qualify for the credit.

- Eligible expenditure can include expenses (e.g. salaries, overheads, materials consumed, etc.) that are deductible for the purposes of computing corporation tax.

- Expenditure incurred on plant and machinery (P&M) can be classed as qualifying R&D spend. In order to qualify, P&M must be eligible for wear and tear capital allowances and must be used for the purposes of undertaking R&D activities.

- Expenditure incurred on R&D activities outsourced to a third-party or third level institution can be included in an R&D tax credit claim, subject to restrictions (see below for key points).

- Key employees who have been actively involved in R&D activities can benefit from an employee reward

mechanism, effectively allowing them to receive part of their remuneration tax free (see below for key points).

- Companies have 12 months from the end of the relevant accounting period in which to make a claim.

All of the above are subject to certain conditions, which companies should investigate thoroughly with a tax advisor prior to submitting an R&D tax credit claim.

Use of the credit

- In the first instance, the R&D tax credit can be used to reduce a company’s (or group’s) current year corporation tax liability.

- Where a company does not have sufficient corporation tax liability in the current accounting period, it can choose to carry the credit back for offset against the corporation tax liability in the preceding period.

Any remaining excess can be carried forward indefinitely against future corporation tax liabilities.

- Instead of carrying the credit forward, a company may elect to have any remaining excess credit paid as a cash refund by Revenue over three years (complex rules apply). The amount of money that a company can claim under the above cash back mechanism is limited to the greater of:

- i. The corporation tax paid by the company during the period of 10 years prior to the previous accounting period, or

- ii. The sum of the payroll tax liabilities for the period in which the expenditure on R&D was incurred and the period prior, subject to conditions.

Outsourcing R&D

Expenditure incurred on R&D activities outsourced to a third party or third level institution can be included in an R&D tax credit claim, subject to certain rules:

- Payment to a third party is limited to the greater of 15% of the company’s overall R&D spend or €100,000.

- Payment to a third level institution is limited to the greater of 5% of the company’s overall R&D spend or

€100,000.

- The total amount claimed must not exceed the qualifying expenditure incurred by the company itself in the period.

- The company must notify the third party provider in writing that it cannot also claim the R&D tax credit for the work it has been contracted to carry out.

‘Key Employee’ reward mechanism

For periods commencing on or after 01/ 01/2012, key employees who have been involved in R&D activities can benefit from a ‘key employee’ reward mechanism, which effectively allows them to receive part of their remuneration tax free. This is subject to complicated rules and should be investigated thoroughly; some of the key points to note are:

- The employee cannot be a director of, or have a material interest in, the company or be connected to such a person.

- The employee must spend at least 50% of their time on R&D activities (i.e. the conception

or creation of new knowledge, products, processes, methods, or systems) and at least 50% of their emoluments must qualify for the credit.

- The amount of credit that can be surrendered to key employees is capped at the amount of corporation tax due by the company before taking the R&D tax credit into account, i.e. the company must be taxpaying.

- The employee’s effective rate of income tax cannot be reduced below 23%.

- In the event of a reduction in the credit amount following a Revenue audit, the onus is on the company to repay the credit surrendered to key employees.

Buildings and structures

- Companies who build or refurbish buildings or structures for both R&D and other activities may claim an R&D tax credit in respect of the portion (as appears to the Revenue to be just and reasonable) of the construction/refurbishment costs that relate to R&D activities

- A minimum of 35% of t must be used for conducting activities for a 4 year period

- The building must be use for a period of 10 years.

- An R&D tax credit of 25 relevant expenditure can claimed in full in the year which the building is first brought into use for the purpose of the trade.

What is R&D?

While there are many activities carried out by companies that could be considered R&D, identifying and quantifying eligible expenditure for the purposes of the R&D tax credit can often be quite complex. Revenue guidelines state that qualifying R&D activities must:

- Be systematic, investigative or experimental in nature,

- Be carried out within a Revenue approved field of science and technology,

- Involve basic research, applied research or experimental development,

- Seek to achieve scientific or technological advancement, and

- Involve the resolution of scientific or technological uncertainty.

What fields of science or technology qualify for the credit?

Allowable fields of science and technology include:

- Natural sciences –

e.g. food science, software development, chemical sciences, biological sciences.

- Engineering and technology –

e.g. mechanical, material, electronic, electrical, and communication engineering, food and drink production.

- Medical sciences –

e.g. basic medicine, clinical medicine, health sciences.

- Agricultural sciences –

e.g. forestry, fisheries, veterinary medicine.

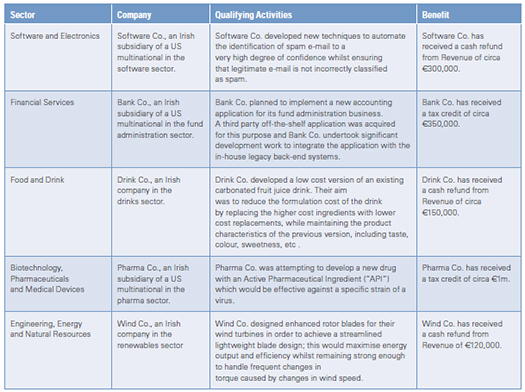

Examples of activities that could qualify for the R&D tax credit

Common errors

- Eligible activities have been overlooked and your claim may be undervalued.

- Your entitlement to claim has not been established properly; this is a complex tax technical area which interacts with other tax legislation.

- R&D activities have not been properly identified and/or documented in accordance with relevant tax legislation and Revenue guidelines.

- Insufficient supporting documentation in place to justify your claim.

- Incorrect inclusion and/or treatment of certain types of expenditure.

- The claim has been filed with Revenue in an incorrect manner.

Implications of an incorrect claim

- Under-claiming – You may not have claimed the full cash value that you are entitled to and are missing out on a valuable refund.

- Over-claiming and/or filing an unsupportable claim – If your claim is audited by Revenue, you may be leaving yourself open to repayment of the credit in addition to interest, penalties and, in extreme cases, publication on the list of tax defaulters.

- Revenue is taking an increasingly hard line with respect to issues arising from R&D tax credit claims. It is therefore very important that all claims should be prepared strictly in accordance with the legislation, tax briefings, e-briefs, Revenue Guidance, practice and precedents.

For more information on the R&D tax credit regime, please contact:

Ken Hardy

Tax Partner

Ireland and EMEA

R&D Incentives Practice Leader

KPMG

D: 01 410 1645

E: ken.hardy@kpmg.ie

1 Stokes Place

St Stephen’s Green

Dublin 2

T: 01 410 1000

F: 01 412 1122

W: www.kpmg.com/ie/en

<< Go Back

|

|

|

|

|

|